News of Intel falling has been drawing traction. This is the company that started the chain reaction in forming Silicon Valley. It’s America’s High-tech icon. Despite initiatives, the USA has been losing an edge in advanced technologies. The latest victim has been the semiconductor that America invented. The issue came to the surface during the recent chip shortage. But is the issue limited to it? If yes, the answer is straightforward, invest in expanding the production.

Interestingly, the problem has a profound root. This is about the loss of Intel’s silicon processing edge to Taiwan’s TSMC. It can no longer produce the smallest Transistor. But this capability has been defining the competition space of the semiconductor industry. Due to it, starting from Apple, Microsoft, Amazon, and Google, one after another anchor customer has been leaving Intel—creating the Intel Falling effect. Instead of using Intel’s chip processed with older technologies, big customers are opting to design their own optimized chips and get them processed with TSMC’s superior process technology.

Ironically, Intel itself has taken refuge to TSMC for producing its main products as competitors like AMD have been taking away Intel’s market share by getting competing chips processed by TSMC’s latest fab technology. But what is the cause behind the reality that Intel Falling? By the way, how did Intel rise as the silicon powerhouse? It seems that the personal computer (PC) wave made Intel the world leader. But it missed the smartphone or mobile wave and a unique model to win the race. On the other hand, TSMC took advantage of it out of the Foundry model, which works far better than Intel’s integrated device-making model (IDM). Ironically, the IDM model made Intel a success story in the PC wave. But the same model is making Intel falling.

Intel rose due to decision failure of IBM and Microsoft’s decision to uplift DOS to Windows:

Gordon E. Moore and Robert Noyce, Silicon valley icons, founded Intel in 1968. It started the journey with memory chip making. However, through an assignment with the Japanese calculator-making company BusiCom, it got into making a small processor 4004—opening an entry in designing and making computer processors.

In the late 1970s, Intel was in memory chip making. Although it had 8080, 8085, 8086, and 8088—a variant of 8086–microprocessors, revenue out of them was negligible. But the situation changed with IBM’s decision to use Intel 8088 as the CPU for its newly designed IBM PC—which debuted in 1981. IBM decided to use an off-the-shelf CPU as the processor of future PC, as the managers did not find a lucrative business opportunity for it. If IBM managers had been able to envision the unfolding future of PC in the 1990s, the decision could have been quite different.

For 8088, Intel had the total in-house capacity for designing, manufacturing, testing, and packaging. It is a model for integrated device manufacturers (IDM). In addition to the growing popularity of IBM PC, Microsoft’s decision to upgrade the text-based Disk Operating System (DOS) to Windows created significant demand to upgrade the underlying Intel CPU. As the graphical user interface of Windows was far more appealing than DOS, users were willing to pay more for the faster speed of the CPU. Hence, Intel found it as an opportunity of turning CPU advancement into a profitable business opportunity. But to improve the performance, Intel had to increase the speed and place more transistors on the same CPU chip. Hence, Intel focused on R&D to improve processing technology, so that dimension of the Transistor keeps falling.

Windows gave a push to Intel process capability:

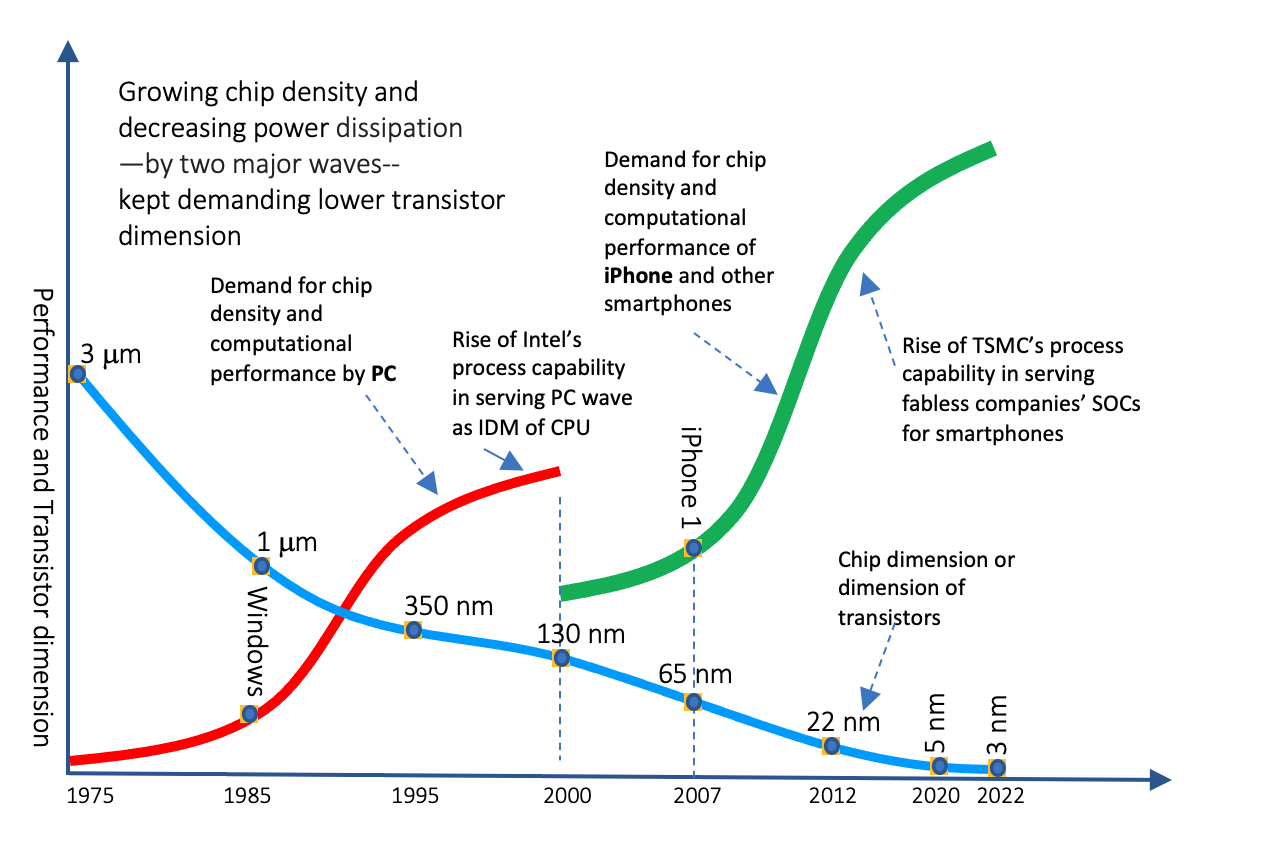

Due to the growing popularity of Windows, innovators were after graphics-intensive applications. As a result, the demand for computing power kept increasing. Hence, it created a virtuous cycle effect on Intel’s R&D investment for increasing chip density by lowering the dimension of the transistor—giving birth to Moore’s law. For example, Intel used a 6 µm process node to make an 8080 processor in 1971. That dimension kept shrinking to 3 µm for 8088 in 1975, 1 µm for 80386 in 1985, and 350 nm for Pentium II in 1995. Consequentially, Intel’s process capability became far ahead of the competition. And Intel maintained this lead till 2017.

However, this advancement kept falling as the PC market kept reducing the return on additional R&D investment of reducing the transistor dimension. Interestingly, another wave was forming for offering increasing RoI for R&D in reducing chip dimension further. It was the smartphone wave—which evolved from simple mobile handsets.

Over the years, chip dynamics have unfolded as a globally distributed value chain. In every major segment, there has been dominance creating a monopolistic scenario.

Intel falling due to its own decision failures:

The computing power required for smartphones jumped into a new wave due to iPhone’s multi-touch technology-based graphical user interface. Hence, during the design of the first iPhone, Apple could not find any off-the-shelf CPUs suitable. Therefore, Apple asked its processor technology supplier Intel. But due to a lack of future prospects, a tight budget, and stress on design and process technology to meet the stringent power requirement of mobile chips, Intel decided not to proceed with Apple’s request. Hence, Apple had no option other than designing the chip and approaching foundry services from a 3rd party. Consequentially, in 2007, Apple ended up with Samsung for using 90nm process technology, one full generation behind Intel’s 65 nm.

The growing popularity of the iPhone’s multi-touch user interface encouraged all other mobile handset makers to imitate such features with Android. But that rapidly increased demand on processors’ computational power. Hence, fabless mobile CPU makers started demanding decreasing transistor size from TSMC—Foundry services providers. Like the past PC wave created out of Windows, smartphones formed a new wave due to the multitouch user interface. It kept demanding a shrinking dimension so that growing chip density could be delivered within the given power consumption budget.

As fabless chip companies like QUALCOMM kept asking for a shrinking transistor dimension for the smartphone SoC (System on Chip), TSMC found it an opportunity of turning R&D into a profitable business opportunity. Hence, TSMC’s aggressive R&D investment kept improving its process capability far faster than others. Consequentially, over a span of little more than ten years, TSMC attained a 5 nm dimension in 2020, while Intel kept struggling to perfect 10nm process technology. Besides, while TSMC has been making a transition to 3nm by the end of 2022, Intel keeps missing deadlines to upgrade to 7nm. It seems that Intel is a few generations behind the global leader.

The consequence of TSMC’s lead and Intel’s Lag led to Intel Falling:

Due to TSMC’s rapid progression in process technology, among many others, Apple migrated from Samsung to TSMC in 2014. Another reason for Apple’s decision was to reduce the risk in the supply chain. Besides, Samsung is a direct competitor to Apple in the smartphone market. In addition to smartphone SoC, Apple has also moved away from Intel’s processor for making its iMac and MacBooks. Apple has used its own in-house design team to design the SoCs for iMac and MacBooks and got them processed by the latest process technology of TSMC. Like Apple, Amazon, Microsoft, and Google have also migrated from Intel’s server chips (like Xenon) to their SoC design and processed them with TSMC’s Foundry services. Furthermore, among the lead users of TSMC’s next-generation 3nm process technology are Apple and Intel, as reported by NikkeiAsia.

Despite having its fab, why has Intel decided to be the customer of TSMC? The answer is simple: the performance of chips produced by TSMC’s 5nm or 3nm process technology is far better than Intel can deliver with its 10nm technology. As mentioned, because of the performance issue, Microsoft, Amazon, and Google have already left Intel and preferred to have their SoC processed by TSMC. Hence, taking TSMC’s fab service is the option that Intel cannot avoid to retain the market of its cash cow chips. For example, as reported by NikkeiAsia, TSMC’s 3-nm technology can increase computing performance by 10% to 15% compared with 5-nm. Besides, smaller transistors delivered by 3nm technology will reduce power consumption by 25% to 30%.

Performance from lower dimensions has been causing Intel Falling:

For the sustaining Innovation edge, Apple has been after decreasing chip dimension. For example, iPhone 12 used 5nm process technology. It’s expected that the next release of the iPhone will use 4nm; and the next iPad will get the processor from the 3nm process. Besides, Intel has been after the 3nm process technology of TSMC. It is crucial for Intel to regain its position in central processing units for notebooks and data center servers which it lost to Advanced Micro Devices and Nvidia over the past few years. Hence, it’s no surprise that in Intel’s history, this is the first time, it will outsource the manufacturing of its core products.

It’s worth noting that Intel’s rival, AMD’s market share for notebook processors, rose from 11% in 2019 to more than 20% last year due to AMD’s adoption of TSMC’s 5-nanometer chip production technology. Besides, Nvidia has been targeting to take away the server chip market from Intel by getting its server chip processed by SMC’s 5-nm tech. Hence, process technology has emerged as a game-changer in the chip business. Furthermore, chip production nanotechnology is not only a commercial pursuit; geopolitics also plays a role.

Power consumption has significant bearings on the competitive edge for mobile handset and tablet PC makers. They cannot simply ask battery makers to keep increasing energy density to meet the demand of increasingly complex SoCs. On the other hand, for cloud service providers, reducing energy footprint highly matters due to operating cooling costs.

Intel’s belated move in Mobile, inappropriate model, and desperate move to be Foundry service provider:

Upon seeing the growing trend of the mobile processor market, Intel made a move to get into this segment. However, it adopted its IDM business model instead of being a fabless or foundry service provider for mobile SoC innovators. Hence, it acquired the mobile phone processor-making division of Infineon Technologies for $1.4 billion in 2011. But due to intense competition from fabless SoC providers like QUALCOMM, the division could not establish a footprint. Intel could not attain significant volume despite desperate attempts to allure customers like LG to use its chips. It seems like Kodak Intel made a mistake due to replicating the past successful model in a different industry.

As a survival strategy, recently, Intel has come up with a massive investment ($20b) in creating additional fabs. Intel has also announced that the Foundry service will be as crucial as IDM. But if Intel cannot uplift the process technology as it’s needed, how will Intel succeed in finding premium customers for its Foundry services? Furthermore, as Intel keeps taking services from TSMC’s latest processes, why should others go to Intel’s Foundry? Does it mean that the game is over, and Intel can never find a top spot in fab maturity? Consequentially, Intel Falling will turn into the new normal, and TSMC-led Taiwan will retain a monopoly.

It seems that the underlying cause of Intel’s falling has been the decision-making failure at the intersection of two waves. By the way, we observed similar situations in the past due to decision failures–creating Kodak or Nokia moment. Ironically, Intel had the right lesson from Andy Grove’s “Only the Paranoid Survive” to prove it wrong.

...welcome to join us. We are on a mission to develop an enlightened community by sharing the insights of Wealth creation out of technology possibilities as reoccuring patters. If you like the article, you may encourage us by sharing it through social media to enlighten others.

Related Articles:

- Semiconductor Value Chain–globally distributed ecosystem

- Semiconductor Monopoly Due to Winning Race of Ideas

- Intel Falling Due to PC and Mobile Waves

- ASML Lithography Monopoly from Sustaining Innovation

- Taiwan’s Semiconductor Monopoly – How did it arise?

- ASML TSMC Nexus Fuels Semiconductor Monopoly

- ASML Monopoly in Semiconductor — where is magic?